On December 29, 2022, the SECURE 2.0 Act was signed into law affecting and reshaping the retirement savings landscape. The Secure 2.0 Act has introduced a range of incentives and provisions aimed at enhancing retirement savings opportunities for both employers and employees. While some of these provisions are effective now, many of the changes will take place over the course of the next three years.

At Servant Solutions, we understand the unique challenges faced by those who have dedicated their lives to serving the church. We are committed to ensuring that the Secure 2.0 Act’s benefits are accessible to our members. We are available to help you navigate this changing landscape, make informed decisions, and maximize your retirement savings potential.

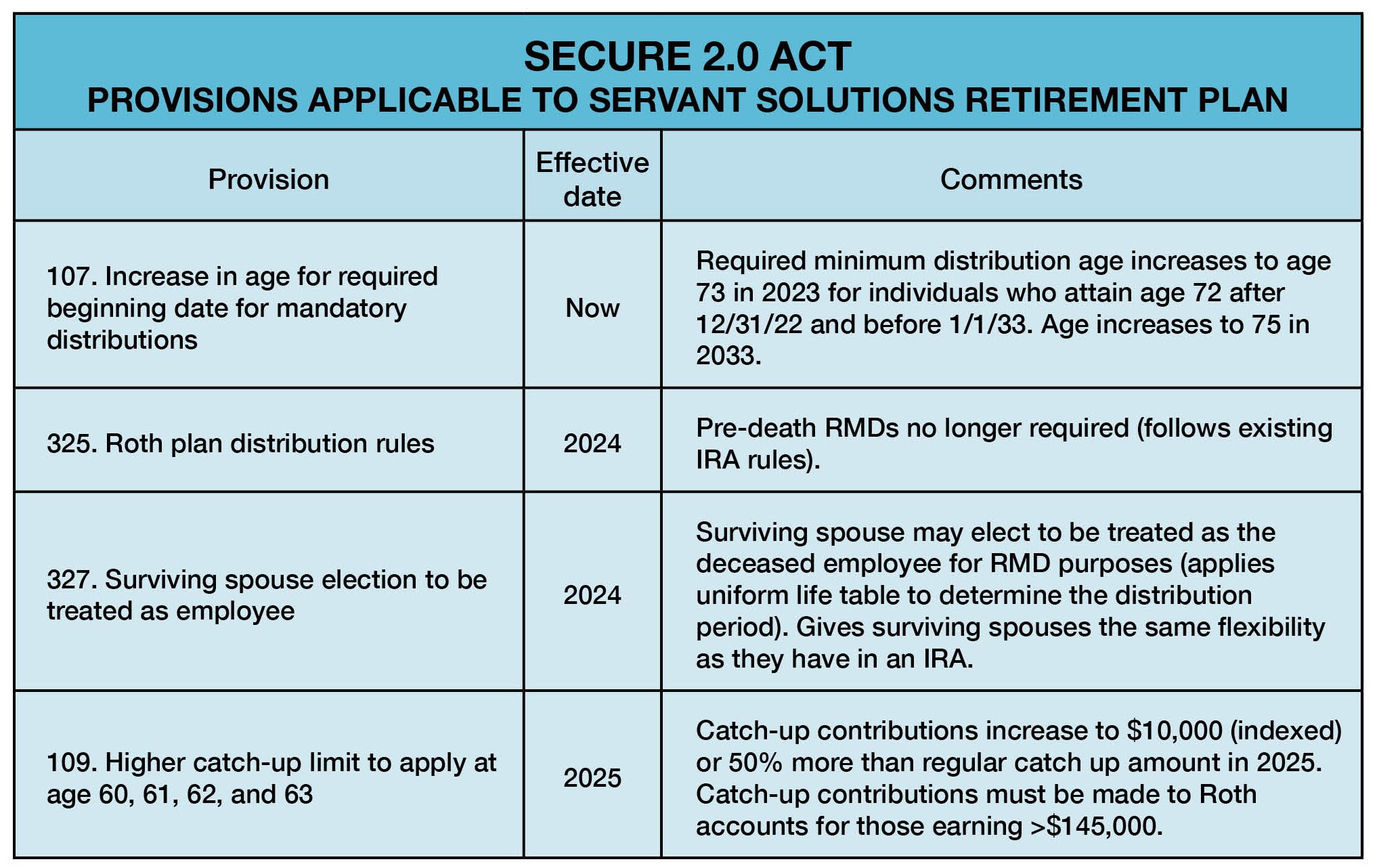

Below are key highlights from the SECURE 2.0 Act that specifically pertain to the Servant Solutions Retirement Plan:.

The required minimum distribution age increased to 73.

An RMD is required if you have an employer-sponsored retirement plan (including 401(k) and 403(b) plans) or a Traditional IRA. No RMD is required for Roth accounts.

No changes have been made to RMD delays; if you are still actively employed for the entire year, you may continue to delay your RMD within that employer’s plan.

Additionally, the penalty for not taking your RMD has been reduced from 50% to 25%.

Save more as you move closer to retirement.

Beginning in 2025, employees ages 60-63 can make catch-up contributions up to the greater of $10,000 (indexed) or 150% of the regular catch-up amount in 2025.

The Saver’s Match will replace the Saver’s Credit.

Unlike the current law that provides for a tax credit for individuals who fall below a certain income level, SECURE 2.0 introduces a federal matching contribution into an IRA or retirement plan for those who are eligible, beginning in 2027. The match is 50% of your IRA or retirement plan contributions, up to $2,000 per individual.

A note about Surviving Spouses:

Effective in 2024, surviving spouses may elect to be treated as the original account holder for RMD purposes (applies the uniform life table which allows for a smaller distribution).

An option for Employers:

Also effective in 2024, employers may elect to offer matching contributions on qualified student loan payments made by employees. Employers who wish to offer this benefit will need to amend their Eligibility and Participation Schedule to reflect the change, allowing employees to self-certify their student loan payments and receive a matching employer contribution to their retirement account.